- Society of Indian Automobile Manufacturers

- SIAM

- Rajesh Menon

- Shailesh Chandra

- auto sales

- car sales

- two-wheelers

- three-wheelers

- commercial vehicles

India’s Auto Industry Rides the Momentum: Record Highs & Renewed Optimism Mark FY 2024-25

- By Nilesh Wadhwa

- April 15, 2025

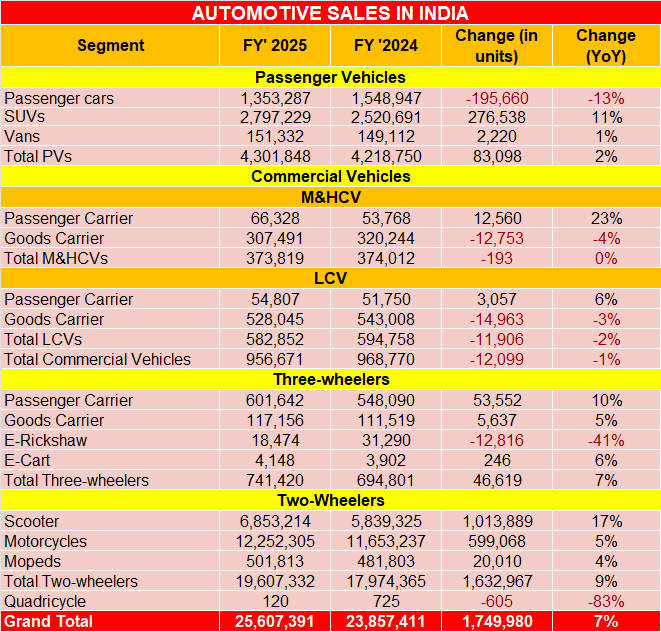

The latest data released by the Society of Indian Automobile Manufacturers (SIAM) show that the Indian automotive industry wrapped up FY 2024-25 with a solid performance, driven by resilient domestic demand, an uptick in exports, and a renewed push toward green mobility.

While the pace of growth varied across segments, the industry overall clocked a healthy 7.3 percent increase in domestic sales, reinforcing its steady recovery trajectory in a post-pandemic economy.

The passenger vehicles segment posted its highest-ever annual sales, breaching the 4.3 million mark – a 2 percent rise over the previous year. Although the high base of FY 2023–24 tempered the growth rate, the segment continued to impress with its scale.

SUVs emerged as the dominant sub-segment, accounting for 65 percent of total PV sales, up from 60 percent last year.

The market responded enthusiastically to new launches and customer demand towards higher ground clearance models. It is also important to note that discounts and promotions kept demand buoyant.

On the exports front, a record 770,000 units were shipped, up 14.6 percent, fuelled by demand from Latin America, Africa and emerging interest from developed markets.

India’s ubiquitous two-wheelers rebounded strongly with 19.6 million units sold, marking a 9.1 percent growth over the previous year. The scooter category led the charge, boosted by improved rural and semi-urban road connectivity.

EV penetration crossed 6 percent, reflecting a growing preference for sustainable options.

Two-wheeler exports rose by 21.4 percent, supported by macroeconomic stability in Africa and expansion into Latin American markets.

The three-wheeler segment on the other hand scaled new highs with 741,420 units sold, a 6.7 percent growth over FY 2023–24. Urban and semi-urban demand for last-mile transport, especially electric models seem to have played a key role.

The commercial vehicles segment posted a slight 1.2 percent decline in annual sales, though Q4 offered a glimmer of hope with a 1.5 percent uptick. Light CVs struggled, while Medium & Heavy CVs (M&HCVs) remained steady. Infrastructure development spurred demand for buses and higher-GVW trucks.

CV exports jumped by 23 percent, indicating global recovery in freight mobility.

In terms of EV sales, the country saw 1.97 million green vehicles sold, up 16.9 percent, with electric two-wheelers seeing a 21.2 percent rise in registrations.

Looking Ahead: Optimism with Caution

The industry body stated that going forward leaders are cautiously optimistic about FY 2025–26. Normal monsoon forecasts are expected to aid rural demand. Recent personal income tax reforms and RBI rate cuts could boost vehicle financing and overall consumer sentiment. Continued export momentum, especially in Africa and neighbouring regions, will offer strategic resilience.

But on the other hand, challenges loom in the form of global geopolitical tensions and evolving supply chain dynamics.

Shailesh Chandra, President, SIAM, said, “The Indian automobile industry continued its steady performance in FY2024–25, driven by healthy demand, infrastructure investments, supportive government policies and continued emphasis on sustainable mobility. Passenger vehicles, two-wheelers and three-wheelers grew in FY2024-25 compared to FY2023-24, but growth rates have been varied across segments. Passenger vehicles and three-wheelers witnessed a moderate growth on account of the high base effect but saw the highest-ever sales in these categories, while the two-wheeler segment registered strong growth in FY2024-25. However, commercial vehicles witnessed a slight degrowth in the FY2024-25, though performance in recent months has been comparatively better. On the exports front, good recovery is seen across all segments, particularly passenger vehicles and two-wheelers reflecting improved global demand and India's growing competitiveness. In FY2024-25, the government of India introduced the PM E DRIVE scheme and PM e-Sewa schemes which underscores the firm commitment of the Government towards promoting sustainable mobility. Looking ahead, the backdrop of stable policy environment, along with recent measures such as reforms in personal income tax and RBI’s rate cuts, will help in supporting consumer confidence and demand across segments.

- Covestro

- FORVIA HELLA

- BMW

- KOLLEKT

- German Federal Ministry for Research

- Technology and Space

- BMFTR

- CircularGlowUp

- Geba

- SW Maschinenservice

- Fraunhofer IEM

- Fraunhofer UMSICHT

- University of Paderborn

- Hamm-Lippstadt University of Applied Sciences

- Helmholtz-Zentrum Dresden-Rossendorf

- Monique Buch

- NALYSES

- Guido Naberfeld

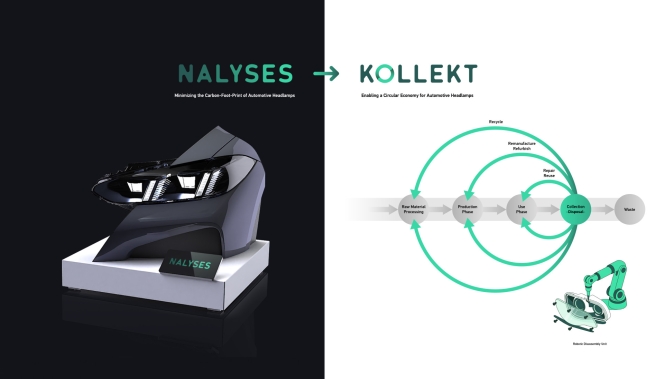

Covestro, BMW & FORVIA HELLA Launch KOLLEKT Project For Recyclable Automotive Lighting

- By MT Bureau

- August 11, 2026

German material manufacturer Covestro has partnered with automotive major BMW, tier 1 supplier FORVIA HELLA, and academic research institutions to launch KOLLEKT, a project focused on developing recyclable automotive lighting and electronic components.

Funded by the German Federal Ministry for Research, Technology and Space (BMFTR) with EUR 4.371 million under the CircularGlowUp framework, the three-year initiative runs from June 2026 to May 2029.

The consortium led by coordinator FORVIA HELLA, includes BMW, Covestro, Geba, SW Maschinenservice, Fraunhofer IEM, Fraunhofer UMSICHT, the University of Paderborn, Hamm-Lippstadt University of Applied Sciences and the Helmholtz-Zentrum Dresden-Rossendorf. The initiative addresses vehicle recyclability, resource consumption and end-of-life material recovery in light of the EU End-of-Life Vehicles regulation.

The project focuses on product design optimised for repair, reuse, remanufacturing and recycling. Covestro contributes its expertise in polycarbonate materials, including its Makrolon, Bayblend and Apec product lines, to evaluate recycling pathways and material properties from the initial design phase.

Monique Buch, Chief Commercial Officer, Covestro, said, “KOLLEKT is a prime example of how we create value together with our customers and partners — going beyond material supply to co-designing solutions from the very beginning. By aligning early across the value chain with BMW, FORVIA HELLA and other partners, we can embed circularity directly into product development. That is what true co-creation looks like—and how we turn sustainability ambitions into tangible outcomes.”

Technological developments within the project include an artificial intelligence-driven robotic dismantling unit. Utilising digital product twins and real-time data processing, the unit aims to enable automated, material-pure disassembly at an industrial scale.

The initiative builds on the predecessor project NALYSES, which concluded in 2026. Project outcomes are intended to support compliance with EU ELV recycling targets through 2032 and assist vehicle manufacturers in meeting post-consumer recycled content quotas.

Guido Naberfeld, Head of Sales and Market Development Mobility, Covestro, stated, “KOLLEKT is a concrete step toward closing the loop on high-performance polycarbonate in automotive applications. By combining Design for Circularity with advanced recycling technologies and digital traceability, we are demonstrating that sustainability and material performance are not a trade-off. This is how Covestro contributes to meeting the EU's ELV targets and helps the entire automotive value chain transition to a truly circular model.”

Mahindra Group Appoints Shveta Arya As Group Chief Strategy Officer

- By MT Bureau

- August 10, 2026

Mumbai-headquartered automotive major Mahindra Group has announced the appointment of Shveta Arya as its new Group Chief Strategy Officer, effective 15 September 2026. Arya will also join the senior management team of Mahindra & Mahindra and serve on the Group Executive Board.

In her new role, Arya will oversee the Group Strategy Office across the organisation's portfolio of businesses to determine growth opportunities and value creation. She will report directly to Dr. Anish Shah, Group CEO & MD of Mahindra Group.

Dr. Anish Shah said, “We are pleased to welcome Shveta Arya as Group Chief Strategy Officer. Shveta brings over two decades of leadership experience across business and strategy, as well as management consulting across diverse sectors. Her experience in driving growth, shaping strategy and leading through change will be valuable as we work with our portfolio of businesses to drive growth and create long-term value across our portfolio of businesses. Her passion for constructive change and holistic progress also resonates strongly with Mahindra’s purpose. I wish her the very best in this key leadership role.”

She comes with over 23 years of experience across publicly listed multinational organisations and management consulting. Her background spans the automotive, travel, financial services and telecom sectors.

Most recently, Arya served as Managing Director of Cummins India, where she managed operations, growth strategy, talent and workplace culture. She was also the program sponsor for Cummins' initiative focused on women and girls in India. Prior to Cummins, she led Strategy and M&A at Thomas Cook India and held roles at Kearney and Infosys.

Arya holds a Master of Business Administration from the Indian Institute of Management Ahmedabad and a Bachelor of Engineering in Information Technology from Delhi University.

Envalior Launches EV Technology Centre Of Excellence At Pune Polytechnic

- By MT Bureau

- August 07, 2026

Envalior India Pvt. Ltd. has launched a specialised training hub focused on electric vehicle technology at MM Polytechnic in Pune, marking a significant step in aligning vocational education with the demands of the burgeoning EV sector. The Envalior Centre of Excellence, a product of the company’s CSR initiatives in partnership with the BroadArks Foundation, is intended to serve as a practical workshop where students can transition from theoretical knowledge to applied technical competence.

The facility was formally inaugurated by Christopher Stillings, Vice President –R&D, in the presence of Krijn Dijkstra, Nileshkumar Kukalyekar, Uday Shetty, Susmita Mishra, Hema Rani, Sainath Vaidya and Aniket Nirwan of Envalior, MM Polytechnic leadership and other dignitaries. By embedding this centre within a technical campus, the programme seeks to immerse learners in the realities of EV maintenance and repair, covering not just mechanical functions but also the intricate electrical and software-driven systems that define modern vehicles.

With an annual capacity to reach roughly 250 learners, the centre will cater to students from ITI and polytechnic backgrounds across multiple engineering streams. The coursework is divided into two progressive phases, starting with a foundational module that introduces participants to basic EV architecture, battery safety and routine service procedures. An advanced tier follows, offering deeper instruction on battery management systems, thermal controls, high-voltage safety protocols, motor controllers and complex diagnostic methods.

Beyond traditional lectures, the training environment incorporates interactive lab sessions with real vehicle components, diagnostic tools and industry-relevant projects, ensuring that participants acquire both safety awareness and problem-solving agility. The overarching goal is to produce graduates who are not merely familiar with EV theory but are confident in executing hands-on repairs and system evaluations. Through this scalable framework, Envalior is actively working to narrow the skills gap in India’s automotive sector, creating a direct pipeline of capable talent for the evolving mobility landscape.

Nileshkumar Kukalyekar, Business Director – South Asia, Middle East & Africa, Envalior, said, “The transition to electric mobility is creating a fundamental shift in the skills expected from the automotive workforce. For us, this Centre of Excellence is about ensuring that technical education keeps pace with that change. By giving students the opportunity to work directly with EV systems, understand advanced diagnostics and build capabilities through structured, certified training, we are helping create a stronger bridge between what young technicians learn and what the industry will increasingly expect from them. We see this as an investment not only in individual careers but in the technical talent that will support India’s mobility transition in the years ahead.”

Christophe Stillings, Vice President – R&D, Envalior, said, "At Envalior, we believe the future of mobility depends on developing industry-ready talent today. Through the Centre of Excellence, students will gain hands-on exposure to EV technologies, helping bridge the gap between academic learning and real-world industry requirements. By bringing together academia and industry expertise, we aim to equip the next generation of engineers with the practical skills, confidence and innovation mindset needed to succeed in a rapidly evolving automotive landscape."

Amit Bhalerao Joins Schaeffler India As COO

- By MT Bureau

- August 07, 2026

Tier 1 automotive supplier Schaeffler India has appointed Amit Bhalerao as its Chief Operating Officer, effective 10 August 2026.

In his new role, Bhalerao will oversee the company's manufacturing operations across India. His responsibilities include directing manufacturing strategy, operational performance, digitalisation projects and capability development, as well as managing local production initiatives across the firm's plant network.

Bhalerao will join Schaeffler India's Executive Leadership Team, collaborating with divisional heads to manage the company's operational footprint.

Harsha Kadam, Managing Director and CEO, Schaeffler India, said, "India continues to be a strategic growth market for Schaeffler, and strengthening our manufacturing and operations capabilities is central to our journey as the leading Motion Technology Company. Amit brings extensive experience in leading complex manufacturing operations, driving operational excellence and building high-performing teams. His leadership will further enhance our manufacturing competitiveness, customer focus and innovation capabilities as we continue delivering greater value to our customers and stakeholders. We wish Amit the very best and many successes in his journey at Schaeffler in India."

Bhalerao comes with 23 years of management experience in manufacturing, operations, lean transformation, quality assurance and supply chain management. Before joining Schaeffler India, he held the positions of Managing Director and Vice-President of Operations at Kelvion India, where he managed operations, technology transfer and capacity expansion projects. He has also held leadership positions at Cummins, Eaton and Sterlite Technologies.

Comments (0)

ADD COMMENT