Outlining the journey of M&HCVs for the last 12 years and how they have reflected IIP growth in India, Jayesh Shelar, Head – Product Management Group, Mahindra Truck & Bus Division, Mahindra & Mahindra Ltd, mentioned, “The last decade was one of discovery and presented key challenges like the 3 emission cycles. The BS IV to BS VI emission norm transition was the fastest in the world.” In his presentation as part of the webinar organized by S&P Global Mobility- formerly IHS Markit Automotive- (as part of their 2022 Automotive Solutions Webinar Series) under the theme ‘Indian MHCV Outlook – Is the Future Truly Electrifying’, Shelar expressed that the industry recovered quickly at a GACR of almost 14.8 percent – from the slowdown of FY2014 to the high of FY2019 – by displaying resilience and strong fundamentals. He spoke about the challenge posed by railways starting from 2010. “The rising fuel prices, a shift towards eco-friendly logistics, and an increase in technology have pushed the vehicle cost up,” he added.

Describing the journey of M&HCV segments as a decade of discovery to a decade of disruption, Shelar said, “There were limited brands in India in 2010. By 2030 there will be multiple brand options available.” Drawing attention to a change in the customer profile, he mentioned, “The entry and exit barriers have come down and will ease further. From being acquisition and resale value sensitive in 2010, customers are now looking at Total Cost of Ownership (TCO). They are ready to experiment with new technologies and brands.” Pointing at a shift to higher capacity engines, Shelar said, “A movement towards battery-operated vehicles is also taking place. Fuel cell technologies are catching up and power requirements are ignificantly going up.” Of the opinion that average speeds have gone up and regulations and infrastructure have improved, he informed, “Trucks are traveling up to 450 km a day as compared to 275 km in 2010. By 2030, they will travel up to 700 km per day.”

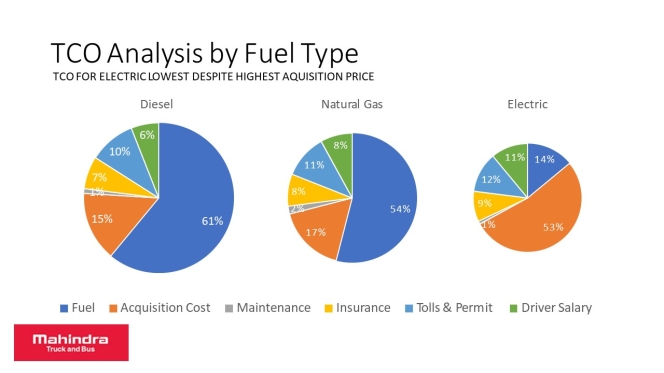

Highlighting rising affinity for technologies like telematics, Shelar mentioned, “A shift from transport to logistics model is taking place.” He drew attention to the TCO of an electric vehicle (despite high acquisition cost) being lower in comparison to the running cost of a diesel and natural gas vehicle over five years. “Fuel cost in diesel and natural gas vehicles is about 55 to 60 percent whereas, in case of the electrical vehicle, it is 14 percent,” quipped Shelar. Underlining the government’s pledge to be net zero by 2030 through measures like 500 gigawatts of non-fossil fuel electricity generation and an increase in natural gas production among others, he said, “Electric vehicle technology is relevant event though issues like high initial acquisition price and charging time will take some time to resolve.”

Drawing attention to key drivers like the FAME policy, stringent emission norms, higher compliance cost, and new business models against challenges like the high initial acquisition cost of EVs, range anxiety, developing charging infrastructure, and battery performance, Shelar said that fuel cell is the long-term technology for M&HCVs. In his presentation, Paritosh Gupta, Analyst – M&HCV Forecasting, S&P Global Mobility, averred that the global M&HCV industry headwinds include the Russia-Ukraine conflict and supply chain constraints. “The forecast for 2022 alone is a drop of about 150,000 units, which is 4.4 percent of the entire market size,” he added. Informing that major degradation has come from Europe and North America, Gupta mentioned, “In 2022, the European and North American markets have dropped by 86,000 units and 38,000 units respectively. A lot of volume from central and eastern Europe has been lost and the possibility of sales moving up smartly in the next three years is less.”

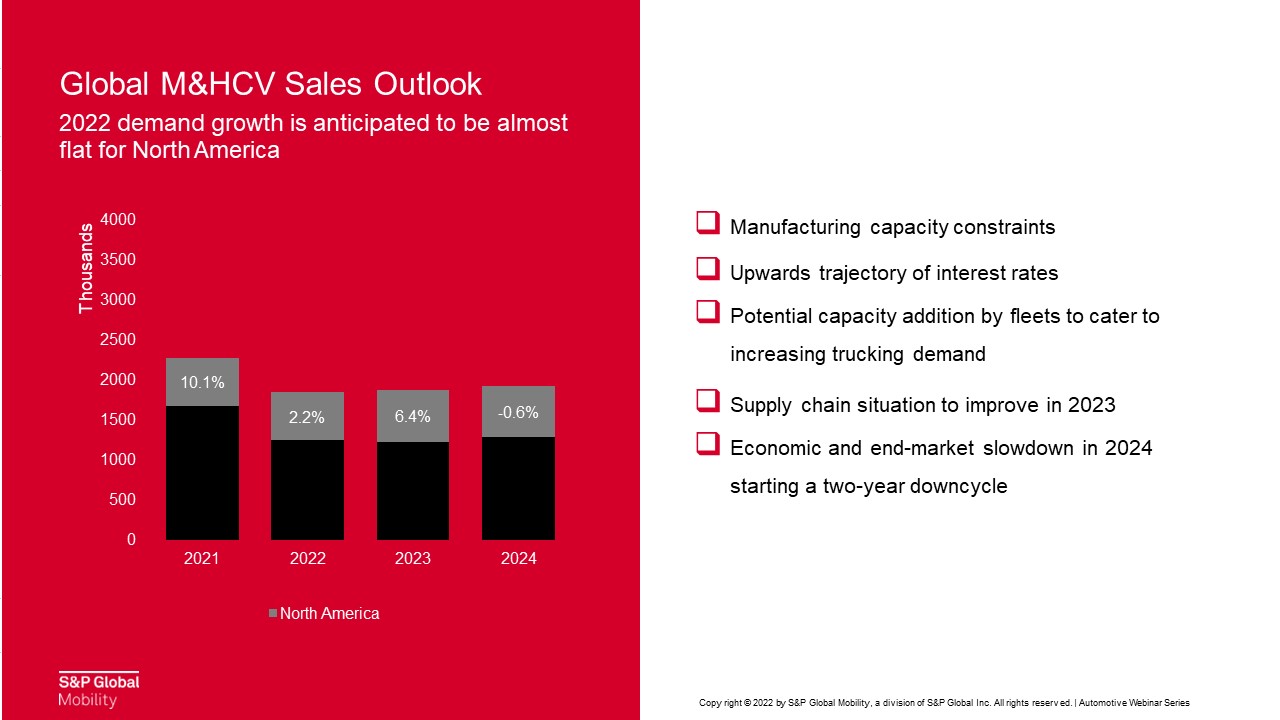

Stating that South Asia, Middle East, and African regions are showing optimism, he explained, “The South Asian market is primarily driven by the performance of the Indian market over the last two quarters. The Chinese market was the only one in 2020 among the key regional M&HCV markets to report positive growth numbers.” Underlining China’s slowing economic growth due to factors like a highly stringent pandemic policy, ithdrawal of pandemic state support, and a shift from road to rail for bulk materials, Gupta expressed, “A 26 percent drop in 2022 and another 1.6 percent drop in 2023 is expected before recovery starts in 2024,” Announcing that the North American forecast is largely positive even though the potential for growth remains limited, he stressed on rising inflation, increasing interest rates, and manufacturing constraints. “We expect fleets to add capacity with the supply chain situation improving in 2023,” quipped Gupta.

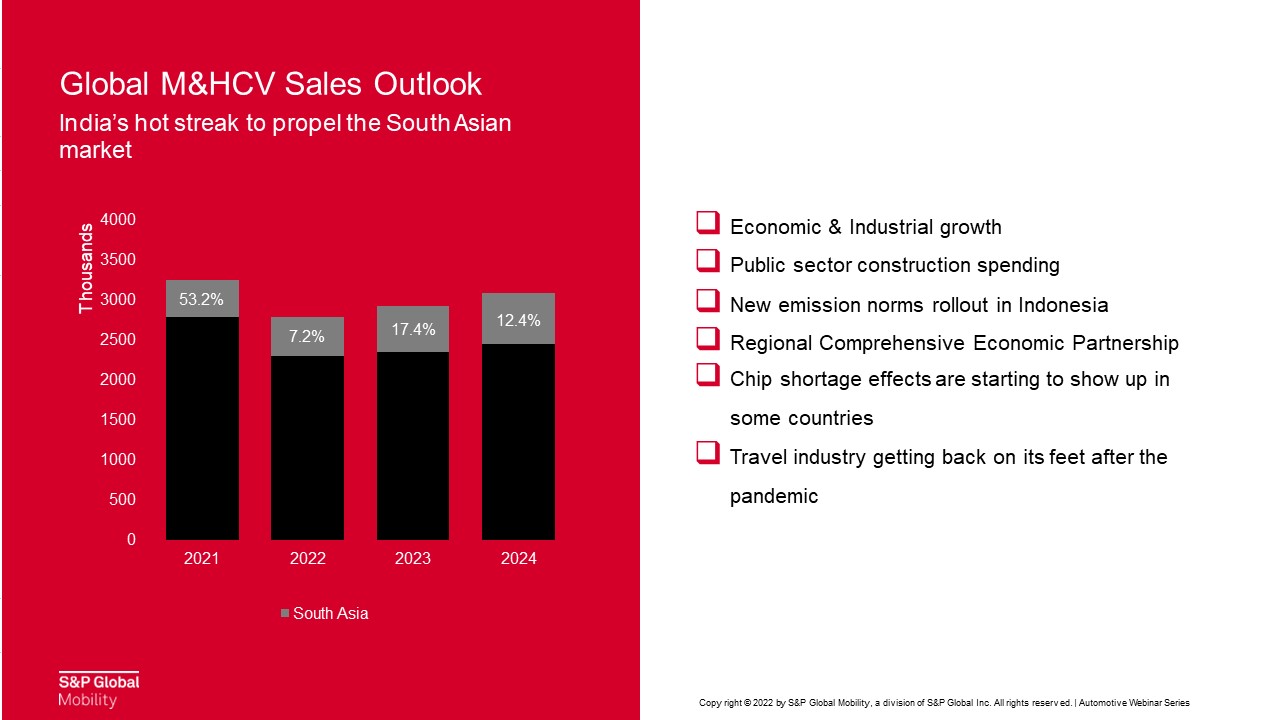

Describing that the Western European market is estimated to remain flattish while the Central and Eastern European market is estimated to drop by 28 percent, Gupta pointed at the Russia-Ukraine conflict and supply constraints as the reasons. Western European markets are facing challenges like raw material and truck price increase whereas the Eastern-Central European markets are facing sanctions, stoppage of production by foreign OEMs, and the possibility of Chinese OEMs setting up shops in Russia, he said. Stressing that South Asia was the fastest growing market in 2021, led by India outgrew expectations, Gupta revealed that India accounts for around 60 percent of the M&HCV sales in the region. “In 2022, the South Asian M&HCV market should grow by 7.2 percent and the figures for 2023 and 2024 will be healthy double-digit ones,” he explained. Of the opinion that the factors driving the South Asian M&HCV market include economic and industrial growth, public sector construction spending, the roll-out of new emission norms in Indonesia, comprehensive economic partnership across the region, and an increase in travel, Gupta quipped, “Struggling with chip and other raw material shortage, the Japanese and South Korean markets are expected to be largely flat.”

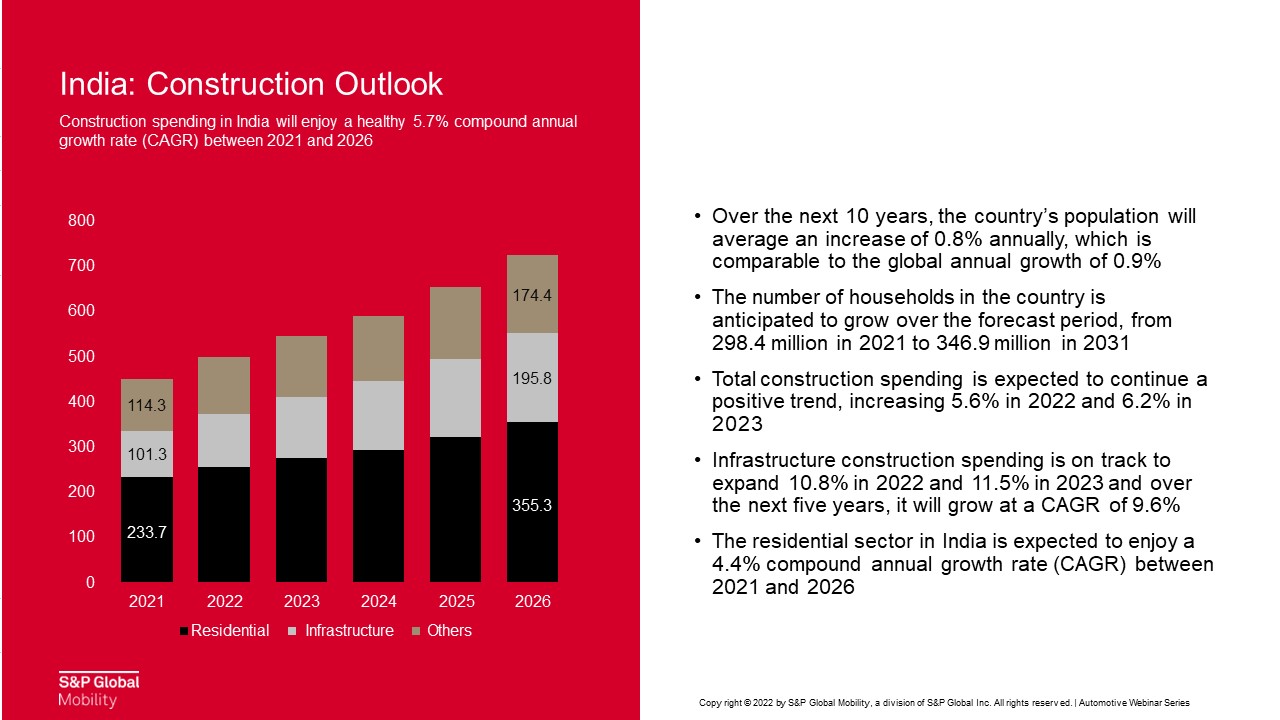

Highlighting rising inflation, high import bills, and weaker global demand as Indian M&HCV headwinds, Gupta mentioned, “The outlook is largely positive though not to the extent it was two years back.” “The construction industry spending will command a CAGR of 10.1 percent between 2021 and 2026 and provide a solid impetus for M&HCV growth,” he added. Stating that while the infrastructure segment’s growth will fuel the growth of heavy-duty trucks, Gupta quipped, “The upward growth trajectory of the e-commerce industry towards becoming the second largest by 2034 is indicative of the growth in demand for medium-duty trucks.” Explaining that the rise of e-commerce and medium-duty trucks over the last five years is a parallel journey, he averred, “Expected to grow at a CAGR of 21 percent over the next 8 years as per IBEF, the e-commerce industry will give a huge boost to medium-duty trucks in India in the future.” “The government has also introduced several policies which are aimed at providing growth to the automotive industry,” he added.

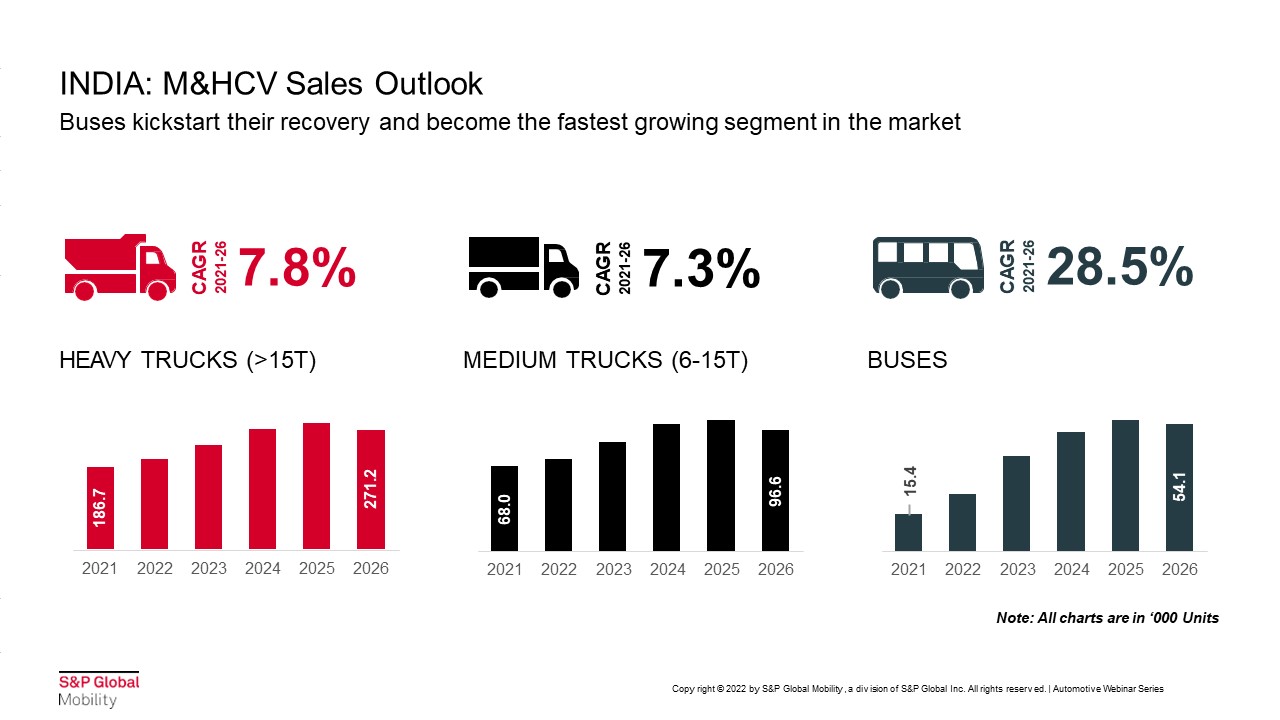

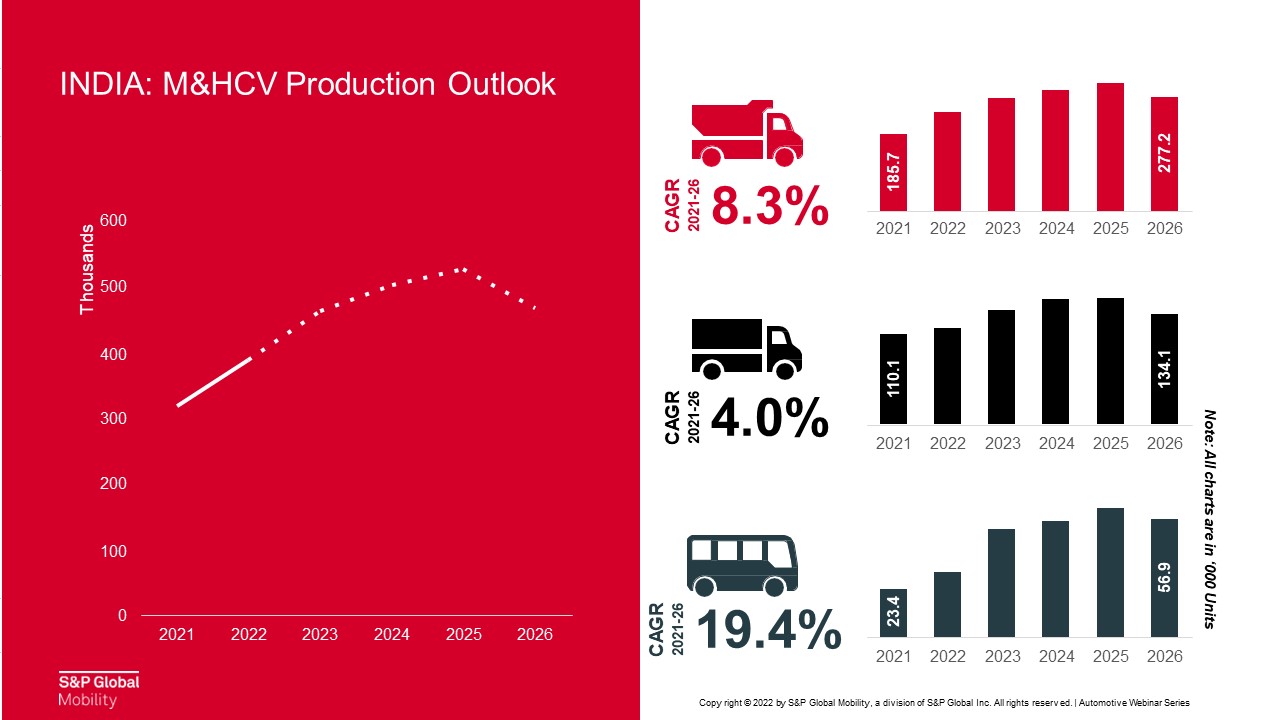

Pointing at the scrappage policy, production-linked incentive scheme, and electrification initiatives, Gupta said, “We see a big tranche of about 50,000 e-buses to come over the next five years” Of the opinion that the monopoly of Tata Motors and Ashok Leyland will continue over the next decade, he averred, “Expect the industry volumes to peak in 2025. Tata Motors will almost touch 200,000 units in 2026.” “In terms of segmental sales, heavy trucks are the largest shareholder in the (M&HCV) market and are expected to clock 275,000 units in 2026 growing at a rate of 7.8 percent,” quipped Gupta. Explaining that MCVs rise will be linked to the rise of e-commerce industry growth and will clock almost 97,000 units by 2026 at a rate of 7.3 percent, Gupta said, “Worst hit by the pandemic, the M&HCV bus segment is expected to pick up in 2022 and reach 54,000 units by 2026.” “The production trend of M&HCVs will be similar to the demand trend in the market. Some buffer will be provided by exports as part of the PLI scheme,” he added.

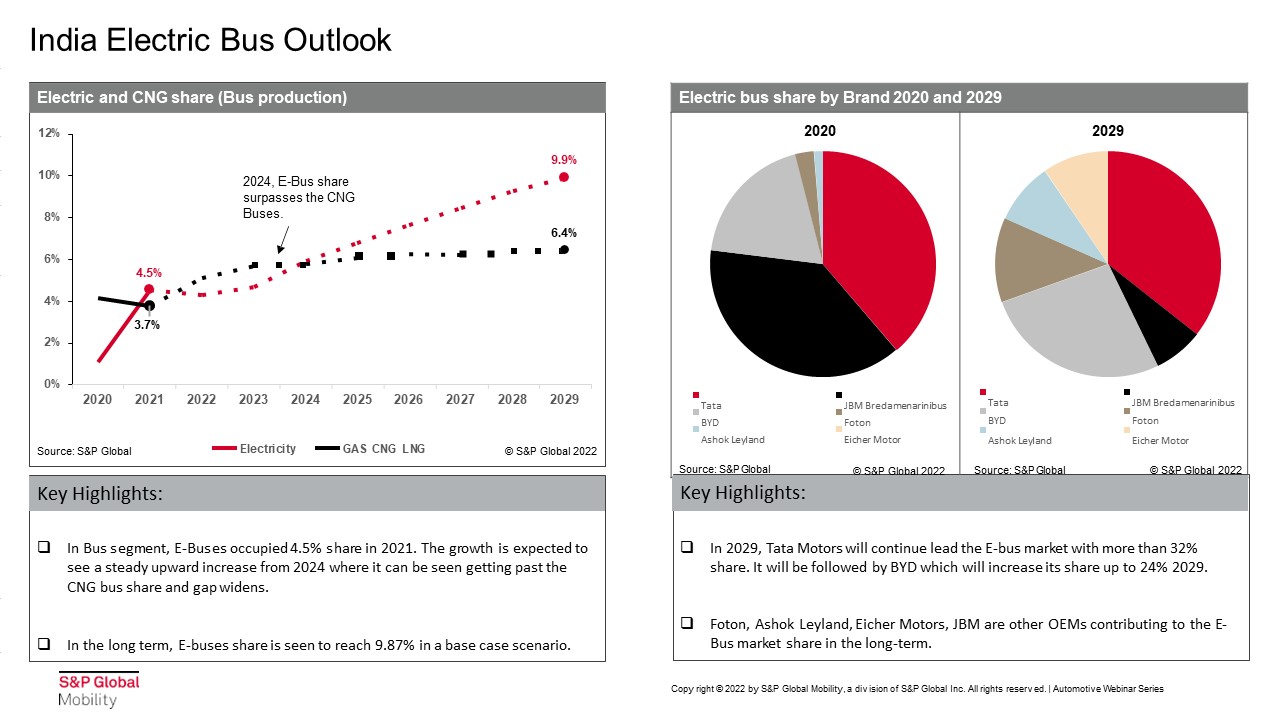

On the topic of M&HCV propulsion trends, Manat Bali, Research Analyst, S&P Global Mobility, mentioned, “Electrification is happening at a much higher pace in buses than trucks. About 99 percent of the M&HCV truck market is currently belonging to IC engines comprising gas and diesel fuels. About 75 percent of the bus market is driven by IC engines running on gas and diesel. With electrification initiatives, the market share of e-buses is expected to reach 30 percent in the long run. It will reach about 9.8 percent by 2029. Natural gas market share will increase up to 12 percent by 2029, triggered mainly by increased availability. It will achieve better traction in medium-duty trucks rather than in heavy-duty ones.”

Of the opinion that diesel fuel will see a de-growth of about 9 percent by 2029 in the Indian CV market at the cost of gas and electrification, Bali averred, “The only electrification taking place in the M&HCV segments is in the bus space as of now. In the long-run, the CNG market share will continue to trail that of the e-bus market share.” “Tata Motors will continue to lead the e-bus market followed by BYD and others in the long run,” he added. About the global e-bus market in the M&HCV category, Bali mentioned, “China is a highly ature and dominant player in e-buses. Other regions are moving up with South Asia having a CAGR growth of 46 percent from 2020 to 2029. India will dominate the e-bus market in South Asia by contributing to over 90 percent of the share.” “The factors driving electrification in India include FAME, state schemes, COP26 target, PLI schemes, and taxation,” he added. “The hindrances in electrification include regulatory drawbacks, infrastructure issues, cost concerns, and end-user dilemmas,” Bali concluded.

Recorded webinar session Available on Demand, please click the link below to watch the session:

https://event.on24.com/wcc/r/3673674/7F886C4E4B36403DD80C623612674EFF?partnerref=motoringtrends

Force Motors Partners Ministry of Road Transport & Highways For Delhi-NCR Vehicle Scheme

- By MT Bureau

- June 30, 2026

Pune-headquartered Force Motors has signed a Memorandum of Understanding (MoU) with the Ministry of Road Transport & Highways (MoRTH) to participate in the Commercial Vehicle Replacement Scheme for the Delhi-NCR region.

The scheme facilitates the replacement of BS-IV and older trucks and buses in Delhi-NCR with BS-VI or electric vehicles to lower emissions. Under the agreement, Force Motors will provide benefits to customers through its dealership network in the region.

Prasan Firodia, Managing Director, Force Motors, said, "Force Motors is pleased to partner with the Government of India in this important initiative to modernise the commercial vehicle fleet in the Delhi-NCR region. The scheme aligns with our commitment to delivering cleaner, more efficient mobility solutions. We look forward to enabling fleet operators and customers to transition to the latest generation of commercial vehicles through this collaborative initiative."

Ashok Leyland Opens New LCV Dealership In Maharashtra

- By MT Bureau

- June 30, 2026

Chennai-headquartered automotive major Ashok Leyland has inaugurated a new dealership for Light Commercial Vehicles (LCVs) in Ratnagiri. This facility is the 16th LCV dealership in Maharashtra, adding to a distribution network of 950 touchpoints across India.

The new dealership is operated by Lavekar Motors as a 3S (Sales, Service and Spares) facility, which features 8 service bays and is located near Mahanagar CNG Pump.

Viplav Shah, Head – LCV Business, Ashok Leyland Ltd. said, “Maharashtra has always been an important market for us, and we are excited to further strengthen our presence in this region. Our relationship with customers is built on trust, performance, and shared growth. Our products are known for their superior mileage, reliability, and performance with a robust network and an industry-leading service retention, we take pride in the continued confidence our customers place in us. The opening of this new dealership marks yet another step in our commitment to delivering world-class products and unmatched services to our valued customers.”

Till date, Ashok Leyland has sold over 600,000 LCVs in India, which are manufactured at the Hosur plant.

Stoneridge To Showcase EVO ECU Platform, Innovation Truck At IAA Transportation 2026

- By MT Bureau

- June 30, 2026

US-headquartered electronic systems and technology company for commercial vehicles, buses, coaches, and off-highway equipment, Stoneridge, has announced its participation in IAA Transportation 2026.

The company is set to exhibit the EVO ECU platform, an electronic control unit designed to support the transition to software-defined vehicles (SDVs). The unit provides processing capability and connectivity, intended to manage vehicle complexity while reducing integration efforts and system costs.

Natalia Noblet, President and CEO, Stoneridge, said, “IAA Transportation will provide our first opportunity to showcase the significant advancements we have invested in to support our customers’ evolving needs. Our investments in engineering, software development, and customer-focused innovation are enabling us to deliver solutions that improve safety, simplify vehicle integration and increase operational efficiency.”

Stoneridge will also feature its Innovation Truck, a demonstrator vehicle equipped with an integrated vision solution and connected tractor and trailer technologies. The display follows the MirrorEye Camera Monitor System, for which the company has produced over 150,000 units. The demonstrator serves to show the integration of the company's technology portfolio for driver awareness and fleet operations.

Christian Leblanc, Global Vice-President of Product and Project Management, Stoneridge, said, “Vehicle architectures are evolving rapidly as manufacturers seek greater functionality, flexibility, and efficiency. EVO ECU has been designed to address these challenges by providing a high-performance platform that simplifies integration while enabling future expansion for emerging safety, security, and connectivity applications. Equally as importantly, the platform has been designed with commercial vehicle manufacturers in mind. It provides the scalability required to support future innovations while helping customers reduce complexity throughout sourcing, validation, and deployment.”

Stoneridge employs approximately 3,200 people. Its European operations include offices and technology centres in Sweden, the Netherlands, Estonia, France and the United Kingdom.

New Holland Launches HD And XHD Series Rotary Tillers In India

- By MT Bureau

- June 23, 2026

New Holland, a brand of CNH Group, has expanded its farm mechanisation portfolio in India with the launch of its new HD and XHD Series Rotary Tillers (Rotavators). The new range is manufactured at the company’s facility in Pune.

The equipment is designed for diverse soil types and agro-climatic zones, aiming to improve soil preparation, productivity, and field performance. A high swing diameter facilitates deeper tillage, improving seed-to-soil contact. The heavy-duty multi-speed gearbox allows farmers to adjust operations based on specific soil conditions, which the company states helps optimise fuel use and save time. The units incorporate Metal Twin-Faced (MTF) seals to protect the rotor hub from water ingress, and utilise DTM paint technology for corrosion resistance.

Tarun Khanna, Director Marketing (AG) India, New Holland, said, "Farm mechanisation is increasingly becoming a key driver of agricultural productivity and efficiency in India. As farmers look for equipment that can deliver superior performance, durability and operational efficiency, the demand for reliable mechanisation solutions continues to grow. The launch of our HD and XHD Series Rotary Tillers reinforces New Holland's commitment to supporting Indian farmers with advanced implements that are engineered for demanding field conditions and designed to enhance productivity."

Following the national unveiling at the company's Greater Noida facility, New Holland plans to introduce the range through a series of dealer-level launches across India. This release is part of the brand’s broader strategy to offer a comprehensive suite of agricultural implements to support modern farming practices.

Comments (0)

ADD COMMENT